HB 1425: Necessary Regulatory Reform

that Will Protect Consumers and Lower Prices

Executive Summary

- The Supreme Court recently ruled that many occupational licensing boards may be sued for engaging in anti-competitive practices. Approximately two dozen of Mississippi’s boards are vulnerable to lawsuit.

- There are, essentially, three ways to protect our boards from legal action: 1) place them under active state supervision; 2) reduce the boards to having only an advisory role; or 3) reconstitute board membership so as to remove members currently practicing in their respective field.

- The Court, as well as the Federal Trade Commission and both the previous and current White House administrations, is skeptical that unrestrained occupational licensing serves the public interest.

- Occupational licensing drives up prices, limits opportunities for workers and, in some cases, originated in prejudicial attitudes aimed at keeping African Americans out of select professions.

- HB 1425 is narrowly tailored to address the concerns raised by the Supreme Court and will protect state occupational licensing boards from frivolous lawsuits while encouraging licensing boards to respect free market principles.

Full Analysis

“Government has nothing to give anyone except what it first takes from someone else,” reads Principle 5 of Governing by Principle. For this reason, the best way for government to foster prosperity is to remove barriers to opportunity rather than directly intervene in the economy. Some of these barriers include a lack of education and job training, high taxes, and heavy regulatory burdens. These barriers kill the dreams of entrepreneurs before they even take flight.

While lawmakers in Mississippi have done an admirable job in recent years of advancing educational opportunity and cutting taxes, the challenge of regulatory reform remains. The basis of government regulation is the responsibility to protect public safety, health and welfare. These are broad categories that easily lend themselves to abuse. So is there a limit to government regulation?

High Court Places Limits on Occupational Licensing Boards

The U.S. Supreme Court has weighed in on this question, determining that regulatory practices that give industry participants an unfair market advantage are impermissible. Explained the Court in its recent N.C. Dental Board v. FTC case:

Federal antitrust law is a central safeguard for the Nation’s free market structures. In this regard it is “as important to the preservation of economic freedom and our free-enterprise system as the Bill of Rights is to the protection of our fundamental personal freedoms.” The antitrust laws declare a considered and decisive prohibition by the Federal Government of cartels, price fixing, and other combinations or practices that undermine the free market.

On the basis of these principles, the Court held that occupational licensing boards that are controlled by “active market participants” (that is, people who currently practice in the profession or occupation regulated by the board) do not enjoy sovereign immunity (immunity from lawsuits) unless the boards are under the “active supervision” of the state. Cautioned the Court:

Limits on state-action immunity are most essential when the State seeks to delegate its regulatory power to active market participants, for established ethical standards may blend with private anticompetitive motives in a way difficult even for market participants to discern. Dual allegiances are not always apparent to an actor. In consequence, active market participants cannot be allowed to regulate their own markets free from antitrust accountability. … Parker immunity requires that the anticompetitive conduct of nonsovereign actors, especially those authorized by the State to regulate their own profession, result from procedures that suffice to make it the State’s own.

In short, the Court has ended the practice of unaccountable boards being given free reign within their own sphere. If boards are going to be comprised of “active market participants” that directly benefit from the regulations they impose, especially if those regulations keep competitors out, these boards must be made accountable to state government. And while the Court allows for some leeway in how this supervision is carried out, “the State’s review mechanisms [must] provide ‘realistic assurance’ that a nonsovereign actor’s anticompetitive conduct ‘promotes state policy, rather than merely the party’s individual interests.’” At a minimum, these mechanisms must meet the following standards:

- The state’s review must be substantive and not merely a procedural rubber stamp;

- The state “must have the power to veto or modify particular decisions”;

- The state may not itself be “an active market participant”;

- Regulatory actions must be based on a “clearly articulated state policy” that implies state endorsement of the action.

What’s Wrong with Occupational Licensing?

The Supreme Court has been relatively tolerant of a variety of regulatory schemes (e.g., Wickard, Chevron, Whitman), which makes the N.C. Dental Board decision all the more significant. While the case may have further implications for other regulatory actions, it most immediately applies only to occupational licensure.

The textbook definition of occupational licensure is that it “is a form of government regulation requiring a license to pursue a particular profession or vocation for compensation. Government licensing generally entails the creation of a licensing board that sets standards for entry into the profession and demands fees to sustain its regulatory activities. Consumers are familiar with licensed professionals, like doctors and lawyers, but do not realize that many other trades require a license or that activities licensed in one state are often not licensed in another.

According to a 2015 White House report on occupational licensing:

- Estimates suggest that over 1,100 occupations are regulated in at least one State, but fewer than 60 are regulated in all 50 States, showing substantial differences in which occupations States choose to regulate. For example, funeral attendants are licensed in nine States and florists are licensed in only one State.

- The share of licensed workers varies widely State-by-State, ranging from a low of 12 percent in South Carolina to a high of 33 percent in Iowa. Most of these State differences are due to State policies, not differences in occupation mix across States.

- States also have very different requirements for obtaining a license. For example, Michigan requires three years of education and training to become a licensed security guard, while most other States require only 11 days or less. South Dakota, Iowa, and Nebraska require 16 months of education to become a licensed cosmetologist, while New York and Massachusetts require less than 8 months.

In a rare case of agreement between the Obama and Trump administrations, acting Federal Trade Commission Chairman Maureen Ohlhausen is creating an Economic Liberty Task Force to address burdensome occupational licensing requirements. Ohlhausen explains:

The public safety and health rationale for regulating many of those occupations ranges from dubious to ridiculous. … Market dynamics will naturally weed out those who provide a poor service, without danger to the public. For many other occupations, the costs of added regulation limit the number of providers and drive up prices. These costs often dwarf any public health or safety need and may actually harm consumers by limiting their access to beneficial services. Other evidence suggests that such regulations are unnecessary or overly broad.

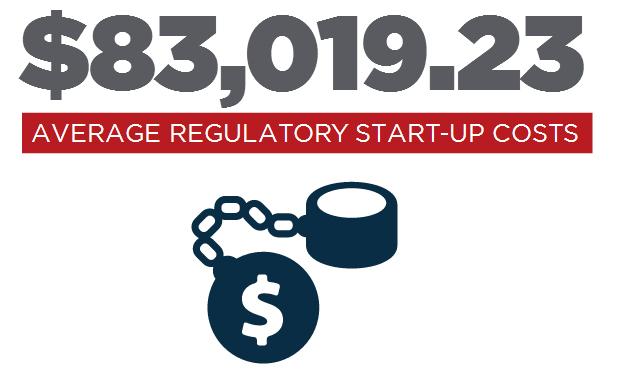

Mississippi regulates a high number of professions. A review by the Institute for Justice found that Mississippi licenses 55 out of 102 mid-to-low-level professions. We license court clerks (only 3 other states do that); residential drywall installers (8 other states); and landscape workers (9 other states). Somehow, nearly every other state manages to get by without licensing these trades.

Numerous studies have demonstrated that, by and large, occupational licensing has no correlation with public safety, health or welfare. Observes the White House report:

Licensing laws also lead to higher prices for goods and services, with research showing effects on prices of between 3 and 16 percent. Moreover, in a number of other studies, licensing did not increase the quality of goods and services, suggesting that consumers are sometimes paying higher prices without getting improved goods or services. … Most research does not find that licensing improves quality or public health and safety.

In fact, the licensing of some professions has more ominous roots. According to research by the Cato Institute:

Before the Second World War, black Americans were increasingly successful in becoming plumbers, barbers and electricians. Trade unions convinced states legislatures to pass laws that made it difficult for them to gain licenses. … By 1941, all of the states of America except Virginia and New York had passed licensing laws obstructing black men who wanted to become plumbers, barbers, and/or electricians. The laws exploited the fact that black people tended to be less well educated and poorer to exclude them from these trades. Simply by being required to pass written exams and pay for courses, they were obstructed. … The purpose of such licensing laws may have been to discriminate against blacks or to reduce competition or both. Whichever it was, it was certainly against the public interest.

This is not say that all occupational licensing is racist, but the coincidence between licensing and prejudice suggests just how easily so-called attempts to protect the public welfare can go astray. This subjective nature of many licensing policies is what prompted the Supreme Court to force states to realign their licensing practices with objective standards that protect the public welfare while preserving the free market.

HB 1425: A Restrained Approach to Occupational Licensure Reform

Prompted by the N.C. Dental Board decision, the Mississippi legislature is considering a bill that would meet the standard of “active supervision” required by the Supreme Court. The bill would do the following:

- Create an Occupational Licensing Review Commission comprised of the governor, secretary of state and attorney general;

- Give this commission the authority to “review the substance” of occupational regulations and approve, disapprove or suggest amendments to these regulations, excluding disciplinary actions;

- Articulate a state policy regarding occupational licensing that defines the various types of occupational regulation, promotes competition, and uses the “least restrictive regulation to protect consumers.”

HB 1425 takes a restrained approach toward addressing the reforms required by the Supreme Court. The bill does not call for a total overhaul of the state’s occupational licensing practices. Such an overhaul, suggests the Federal Trade Commission, would entail limiting board activity to an advisory role or restricting board membership to those with no financial interest in the regulated profession.

HB 1425 also does not apply to all boards, but only those controlled by “active market participants.” The bill does not radically expand the governor’s authority over licensing boards, but disperses this review power to other statewide officers.

Again, it is worthwhile recalling that the Supreme Court requires “active state supervision” that is substantive and will be evaluated based on “all the circumstances of the case.” There is no other way to read this guidance than to presume that the state must provide for something like the active review process mandated by HB 1425. All in all, HB 1425 is aligned with a narrow reading of the N.C. Dental Board case that will protect state occupational licensing boards from frivolous lawsuits while also encouraging licensing boards to respect free market principles.

|

Religious liberty is good for the economy, so says a new

Religious liberty is good for the economy, so says a new  "A little understood revolution in American law is taking place- regulation by litigation, which places national lawmaking into the hands of powerful coalitions of state attorneys general (AGs) who have no lawmaking power," reports the Competitive Enterprise Institute about a new paper "

"A little understood revolution in American law is taking place- regulation by litigation, which places national lawmaking into the hands of powerful coalitions of state attorneys general (AGs) who have no lawmaking power," reports the Competitive Enterprise Institute about a new paper "|

|

Honor System for Welfare Not Working

Trust, but verify. Seems like commonsense. Unfortunately, government programs are often lacking in common sense. According to the Miss. Department of Human Services, self-verification is the method used to determine eligibility for Food Stamps, also called the Supplemental Nutrition Assistance Program (SNAP). The director of Fraud Investigation with the department acknowledges: “The application process for SNAP is based on an ‘honor system,’ trusting that applicants truthfully submit their income and number of dependents.” It should come as no surprise that some people aren’t telling the truth about their identity or residency or income when applying for welfare, whether it be Food Stamps or Medicaid. What is surprising, unbelievable really, is that the state is not really verifying who people are, where they live, and whether they are actually in need. The result is millions of taxpayer dollars lost to fraud, waste and abuse. This is savings that could be going to help the nearly 8,000 Mississippians with disabilities and other serious needs on a waiting list for Medicaid’s Home and Community Based Services. It is savings that could be going to patch holes in our Medicaid budget, or state budget.

A bill (HB 1090) moving through the state legislature would require Miss. welfare programs to use a verification service to check for things like identity and residency. Using databases easily accessible in the private sector, this service would discover whether a Social Security number is being fraudulently used. When Illinois ran a similar audit they found 14,000 dead people on their Medicaid rolls. The eligibility review would also check things like whether someone on Mississippi Medicaid is paying property taxes in another state – a likely sign the recipient is not a Mississippi resident. It would check incarceration status and death records and immigration status – all the things any reasonable voter assumes are already being verified to protect the integrity of our welfare programs.

HB 1090 also includes commonsense reforms like expecting SNAP enrollees to cooperate with a fraud investigation. The bill would track where welfare benefits are being accessed and spent. When Maine ran such a check, they found $3.5 million worth of transactions in Florida, including hundreds of thousands of dollars in withdrawals from ATMs near Walt Disney World. When the state of Florida ran such a check, they found 3,500 of their Food Stamp recipients were also receiving Food Stamps in at least one other nearby state, including Mississippi.

Those who claim welfare fraud is not a problem in Mississippi are mistaken. It is so much of a problem that in 2015 the Mississippi Department of Human Services (DHS) was awarded a $1.9 million federal grant to help eliminate fraud. It is so much of a problem that the state auditor has found millions in questionable TANF costs and warned that the “failure to maintain supporting documentation for eligibility as well as not monitoring and reducing benefits” as required could result in the state having to repay federal funds.

Similarly, we have seen recent arrests for welfare fraud in several counties. According to news reports, DHS has been “knocking, one door at a time, looking for people who’ve applied for food stamp benefits that aren’t entitled.” Instead of going door-to-door, we can harness the power of technology to catch a good bit of that fraud with the click of a button.

It is no accident that the states most committed to a robust social safety net are also rooting out fraud most aggressively. The first state to proactively verify its Medicaid rolls was Pennsylvania, which launched its own program in 2011. They identified 160,000 ineligible welfare recipients in the first 10 months and saved the state nearly $300 million. Illinois, Minnesota, and Massachusetts soon followed. Altogether, those four states are seeing a combined savings of $1.3 billion annually. We estimate Mississippi would save $40 million annually, based on a fraud rate of 10 percent.

If we want to protect our Medicaid and other welfare programs for those who are the poorest of the poor, the disabled, the elderly, we need to eliminate fraud and waste. We owe it to all Mississippians – including those who are truly eligible to receive these benefits – to be good stewards of these programs.

Jameson Taylor, Ph.D.

Vice President for Policy, Miss. Center for Public Policy

Combatting Welfare Fraud in Mississippi with Commonsense Reforms

A bill (HB 1090) before the Miss. Senate implements a number of best practices aimed at combatting welfare fraud. The bill would save the state an estimated $40 million [1] annually by verifying eligibility for Medicaid and SNAP/food stamps. The bill also creates oversight procedures – like tracking where EBT (food stamp) and TANF cards are used – to discourage fraud.

Medicaid Fraud

The U.S. Government Accountability Office (GAO) warned again this year, as it has for the past 14 years, that Medicaid is a “high-risk” program owing to “vulnerabilities to fraud, waste, abuse, and mismanagement.” An estimated $60 billion in Medicaid expenditures are thought to be lost to fraud each year. Likewise, according to the National Conference of State Legislatures, “Fraud and abuse in Medicaid cost states billions of dollars every year, diverting funds that could otherwise be used for legitimate health care services.”

There are basically two types of Medicaid fraud: provider fraud and enrollee fraud. While the federal government apparently has no mechanism in place to accurately track fraudulent Medicaid spending, its Centers for Medicare & Medicaid Services estimates that “eligibility errors” account for the majority of payment “errors.”

This suggests that the majority of Medicaid fraud is generated by ineligible recipients. Such recipients are generally misreporting identity, residency, citizenship status and/or income. Identify theft, for example, is rampant in Medicaid. Arkansas recently audited its Medicaid rolls and found 20,000 enrollees with “high-risk” identities, many of them using stolen or falsified Social Security numbers. Illinois conducted a similar review and found 14,000 dead people on Medicaid.

Under federal law, the Miss. Division of Medicaid is supposed to verify eligibility on an annual basis. States have the option of relying on “self-attestation” for eligibility and cross checking this information against a federal database (PARIS) that is supposed to verify Social Security number usage.

In 2016, the PARIS database flagged only 2.4 percent of Mississippi Medicaid recipients as having a Social Security number used by someone in another state. By contrast, other states are finding an average fraud rate of 10 percent after implementing the reforms mandated by HB 1090. These states are using private-sector databases to quickly and inexpensively verify ongoing eligibility.

HB 1090 would require the Division of Medicaid to enter into a competitively bid contract to hire a vendor to monitor ongoing Medicaid and SNAP/food stamp eligibility. The vendor would only be paid out of the savings generated by catching fraud. The vendor would not be able to actually remove anyone from Medicaid or any other welfare program, but would only flag suspicious information, leaving it up to Miss. Medicaid to investigate and handle the removal of verified cases of fraud.

States that have implemented similar monitoring systems have seen a return on their investment of well over 10 to 1. Illinois, for instance, is saving almost $400 million annually. Pennsylvania saved $710 million in 18 months. Minnesota estimates annual savings of $307 million.

At least 11 other states are currently running or have recently run some form of enhanced welfare verification audit: Alaska, Arkansas, Illinois, Kansas, Maine, Massachusetts, Minnesota, Missouri, Pennsylvania, Rhode Island, and Wyoming.

Welfare Fraud & Abuse

The eligibility verification system created by HB 1090 would apply to all Mississippi welfare programs administered by the Division of Medicaid and the Department of Human Services (DHS), including SNAP/food stamps and TANF. Food stamp fraud in Mississippi is a serious problem, if only judging from the many cases of fraud reported in the media. According to a 2012 report in the Daily Journal, “In the last fiscal year alone, 1,705 people were disqualified from Mississippi’s Supplemental Nutrition Assistance Program – SNAP – for making false claims and bilking the program out of more than $2.7 million.” These 1,705 cases of fraud represent 0.2 percent of total enrollment. The actual fraud rate is likely much higher.

“The application process for SNAP is based on an ‘honor system,’ trusting the applicants truthfully submit their income and number of dependents,” acknowledges DHS fraud investigator Ken Palmer. In particular, DHS has found that a number of recipients do not report income, causing “the client to get taxpayers’ dollars that they were not entitled to.”

While DHS’s efforts at catching fraud are appreciated, the department is relying on a “pay-and-chase” model that enables fraudsters to remain on the rolls indefinitely, until and unless they are actually caught. Using existing technology to review welfare eligibility on a quarterly basis would speed up the process of eliminating fraud, saving the state money and sending the message that fraudsters shouldn’t target Mississippi.

In addition to proactively verifying eligibility, HB 1090 reigns in welfare abuse by eliminating several loopholes used by the Obama administration to gut landmark welfare-to-work reforms signed by President Bill Clinton in 1996.

Federal law, for example, requires most working-age (18 to 50) able-bodied, childless adults to cycle off of food stamps after 3 months unless they are working, training or volunteering for at least 20 hours a week. Under a “waiver” offered by the Obama administration, Mississippi dropped this requirement from 2009 to 2016. The state has similar waivers that have eliminated income and asset tests for food stamps. These are still in place.

Kansas is another state that reinstituted the able-bodied adult work requirement, but then tracked 41,000 former recipients to analyze the results. Half obtained employment almost immediately, and almost two-thirds were working within a year. Incomes rose by an average of 127 percent a year, with many finding permanent well-paying jobs in a variety of industries. Other quality-of-life measures, like marriage rates, also increased.

HB 1090 would require legislative permission for Mississippi to again waive food stamp work requirements. The legislature would also have to statutorily authorize any waivers eliminating income and asset standards.

Other states have found good reason to implement the reforms in HB 1090. Michigan discovered it had thousands of lottery winners on welfare. “I feel that it’s OK because I have no income, and I have bills to pay,” admitted one million-dollar winner. “I have two houses.”

Since Michigan, like Mississippi, does not have an asset standard, even multimillion-dollar winners could legally remain on food stamps until public outrage forced a change in law. In Ohio, the millionaire son of an Iranian prince was found to be receiving both food stamps and Medicaid. The man reportedly held $4.2 million in a Swiss bank account, lived in an 8,000 square foot home and had a BMW and Lexus parked in his four-car garage. In his defense, the fraudster claimed, “It was our right to apply [for food stamps] and I applied. If you don’t like the system, change it.” Ohio’s welfare programs, not unlike Mississippi’s, waive asset standards. “I answered every question asked by benefit workers,” claimed the man.

Along with restoring federal welfare-to-work reforms, HB 1090 would provide state policymakers with additional information as to how the state’s welfare benefits are being utilized. Among other things, the bill would track out-of-state welfare usage. When Maine ran such a check, they found $3.5 million worth of transactions in Florida, including hundreds of thousands of dollars in withdrawals from ATMs near Walt Disney World. In turn, when Florida ran such a check, they found 3,500 of their food stamp recipients were also receiving food stamps in at least one other nearby state, including Mississippi. The bill would also codify and expand the list of prohibited ATM (TANF) transactions at liquor stores, casinos and strip clubs to include spas, nail salons and similar locations.

Note 1: A fiscal note from the Department of Human Services, prepared by The Stephen Group, estimates annual savings from Medicaid verification of $6.9 million in General Fund savings and $6.2 million in federal savings from the SNAP/TANF reforms. (Mississippi pays about 25 percent of the cost of Medicaid while the federal government pays about 75 percent. The federal government pays the full share of SNAP/TANF costs, though the state is responsible for administrative costs.) The Stephen Group report assumes a fraud rate of 1 percent for Medicaid managed care; 1 percent for SNAP; and 2 percent for Medicaid long-term care. Other states that have conducted similar reviews have identified much higher fraud rates, depending on the nature of the audit: Illinois (34 percent); Arkansas (ranges between 3, 12 and 24 percent); Minnesota (17 percent). Based on the experience of other states, we anticipate an average eligibility fraud rate of 10 percent of total enrollment, which would be roughly 72,000 cases based on FY2016 average monthly enrollment of 728,704 (excludes CHIP). Not every enrollee costs the same, but annual spending per enrollee in Mississippi is $5,913: the range being $18,592 for the most expensive enrollees to $2,403 for the least expensive. If we use the very conservative estimate of $3,000 per year in enrollee costs (much less than The Stephen Group assumes), we arrive at the following: $3,000 x 72,000 cases divided by 6 months = $108 million. Based on our current FMAP, this translates into $27 million in savings for a half year. If the audit is run twice in a twelve-month period, this number will double to $54 million. Hence, we conservatively assume savings ranging from $27 million to $54 million, the average of which is $40 million. To be clear, the savings other states are seeing is not only from a one-time review of their rolls, but from constant monitoring. We recommend a quarterly audit, resulting in even greater savings. We also estimate there will be some administrative savings as non-eligible individuals drop off of the SNAP/TANF rolls. The Stephen Group report estimates the enhanced eligibility and other reforms will cost about $3 million annually, but expects federal funding to cover as much as two-thirds of this amount. Assuming the cost is even as high as $2 million annually, this would result in a return on investment of 20 to 1.

|

Mississippi’s Internet Sales Tax: The explosion of online retail sales has fostered a debate about whether and how to collect taxes on those purchases from companies that are not currently required to collect them. During the 2017 legislative session, the Mississippi House of Representatives passed a bill regarding this issue. That bill, HB 480, died in the Senate Finance Committee, but the issue itself is not going away. The Mississippi Department of Revenue (DOR) has proposed a regulation very similar to the legislation. A major difference between the regulation and the legislation is that HB 480 would have directed that the taxes collected by certain out-of-state sellers be spent on road and bridge repair. Although there are many aspects to this debate, this paper is intended to explain only a few of the policy matters involved. It does not seek to take a side, but to impartially explain the pertinent facts. For the most part, we will deal with things as they are, not as they should or should not be.

Is this a new tax? Is it a tax increase? The answer to both questions is no, at least as applied to the tax itself. The process to collect the tax will be taxing – logistically, financially, and emotionally – especially for small businesses. But the use tax on the purchase itself is neither a new tax nor a tax increase. Here’s why. For every item you buy right now that is subject to sales or use tax, you are the one who owes the tax. It would have perhaps been more accurate to call it a “purchase tax” than a “sales tax.” The tax is not on the business from which you purchased the item. The tax is assessed on the item itself, and you as the purchaser owe the tax. In order to make it easier to identify and collect the tax, the state requires sellers (retail stores, for instance) to collect it for you. That’s why it’s not included in the price of the product but is identified as a separate item on your receipt. (In contrast, businesses include the cost of their own taxes, such as income or property taxes, in the underlying price of the product, not as a separate item on the receipt.) Consider this analogy. You owe tax on your income. In order to increase compliance, the state requires your employer to withhold money from your paycheck and send it to DOR. That’s not a tax on your employer. You are the one who owes the tax. If your employer doesn’t withhold enough, you still owe the full tax on your income, and you are required to remit it when you file your tax return. In the same way, if a retailer – in-state or out-of-state – collects an adequate amount of sales or use tax for you, you owe nothing more. But if the retailer does not collect it, you still owe it. Whether you have noticed or not, or whether you have answered it truthfully or not, your Mississippi tax return asks you to identify the amount of purchases you made from out-of-state companies for which you did not pay sales or use tax. You are supposed to pay 7% of that amount to the state. Apparently, not many people do that. If you buy an item in another state and the seller charges you sales tax in that state, you can deduct that amount from the use tax you would otherwise owe to the state of Mississippi. The very important exception to this: you cannot deduct sales or use taxes paid in another state on most motorized vehicles (cars, trucks, motorcycles, boats, etc.) whose first use will be in Mississippi. In other words, if you buy one of those items in another state, and it has not been used before, you will owe the full use tax in Mississippi even if you paid sales tax in the state where you bought it.

To summarize: the tax on purchases from out-of-state sellers is a tax that is owed now; it is not a new tax, and it is not a tax increase. If the tax is already owed, what’s the problem with requiring sellers to collect it? If that’s the case, has Congress shown any interest in allowing it? Since Congress has not acted, what governs internet tax collection?

If Congress does eventually pass a bill, what safeguards are likely to be approved for small businesses to deal with the complexity?

Are those safeguards in the proposed DOR regulation? If the U.S. Supreme Court has said states cannot require out-of-state businesses with no physical presence in-state to collect these taxes, why would DOR attempt to do so anyway? For the legislature, the apparent motivation behind HB 480 was to increase the amount of money being directed toward road and bridge repair, by allocating to that purpose the amount of use taxes collected and remitted by out-of-state sellers. Of that amount, 70% would have gone to the state Department of Transportation for state-maintained roads and bridges, and 30% to cities and counties for local road and bridge repair. Normally, the use tax goes into the General Fund, which is the primary source from which the legislature appropriates funds to schools, Medicaid, prisons, etc. Road and bridge funding comes primarily from the tax on gasoline and other fuels, generally referred to as the “gas tax.” Other Common Questions Those who would answer “no” say it is wrong to place the tax-collection burden on out-of-state sellers because the sellers don’t use water and sewer infrastructure, or fire and police protection, or other benefits provided by local and state government to brick-and-mortar establishments. They also say buyers generally choose to purchase online more for convenience than price, so the 7% difference would not change the purchasers’ buying decisions. In addition, they say sales tax collections have not declined despite the rise in online sales. I noticed Amazon is now charging me 7% on the items I buy from them. If they aren’t required to collect tax on their sales to Mississippians, why are they doing so? Do we know whether Amazon is receiving any special benefits as a result of their agreeing to collect a use tax? March 1, 2017

|

(JACKSON, MISS—FEBRUARY 17) – Today, the Mississippi Justice Institute (MJI) filed a complaint with the Mississippi Ethics Commission following a refusal by the Department of Revenue (DOR) to make available public documents related to a voluntary agreement between that agency and the online retailer Amazon. The agreement, as first disclosed in public statements by Department of Revenue officials, appears to provide for Amazon to collect use tax from online purchases from Mississippians and remit those taxes to DOR. DOR officials have publicly spoken of negotiations between the agency and Amazon.

“Mississippi law requires government transparency and accountability. As taxpayers, the public should be allowed to know the details of our state agencies’ agreements and contracts with outside entities – in this case a billion dollar corporation collecting taxes on behalf of the state. These details are particularly important because they involve an issue with current active legislative debate and recently completed but not yet enacted rulemaking by the Department of Revenue. The state is making policy on this issue without revealing public information which could inform the citizens,” said Mike Hurst, director of MJI.

Hurst continued, “The Department of Revenue denied our open records request citing confidentiality of required tax records. But the agreement isn’t a required tax record because this is a voluntary agreement. Under existing U.S. Supreme Court precedent, the Department of Revenue cannot require an out-of-state company with no physical presence in Mississippi to pay a use tax. There is no exemption to Mississippi’s transparency laws which allows the Department of Revenue to deny review of these public records, so we have appealed their refusal to the Ethics Commission,”

Hurst noted several questions the information requested might answer.

- Has the state agency obligated taxpayers to any agreement?

- Did DOR agree with Amazon that, in exchange for voluntarily collecting these use taxes for DOR, DOR would promulgate regulations attempting to codify the application of use taxes to other out-of-state companies?

- Did DOR structure the agreement at Amazon’s request to give Amazon a competitive advantage over competitors?

- Did DOR agree to give Amazon some kind of benefit for voluntarily coming forward and agreeing to collect use taxes for DOR? If so, what are the details of that contract between a state agency and a collection company?

- Did DOR agree to shield third-party sellers on Amazon’s platform from collecting use tax?

You can read MJI's record request here; the DOR's refusal here, and MJI's complaint to the Ethics Commission here.

The Mississippi Justice Institute represents Mississippians whose state or federal Constitutional rights have been threatened or violated by government actions. It is the legal division of the Mississippi Center for Public Policy. To learn more about MJI, visit www.msjustice.org.

--30--

|

|

Regulatory reform is cutting red tape in North Carolina and it can work in Mississippi, too. So says Joe Sanders of the John Locke Foundation in a

Regulatory reform is cutting red tape in North Carolina and it can work in Mississippi, too. So says Joe Sanders of the John Locke Foundation in a  By passing a phase-out of Mississippi's franchise tax, Mississippi Lieutenant Governor Tate Reeves and Speaker of the House Philip Gunn this month received the 2016 Outstanding Achievement in State Tax Reform by the Tax Foundation.

By passing a phase-out of Mississippi's franchise tax, Mississippi Lieutenant Governor Tate Reeves and Speaker of the House Philip Gunn this month received the 2016 Outstanding Achievement in State Tax Reform by the Tax Foundation.

Mississippi Department of Education (MDE) is seeking feedback on revisions to the College and Career-Ready Standards for Science. MDE has created

Mississippi Department of Education (MDE) is seeking feedback on revisions to the College and Career-Ready Standards for Science. MDE has created

|